By Ashley Bleckner, CFP®, MA

Listen up: if you have a high deductible health care plan (HDHP), then you may have access to one of the best retirement vehicles that you’re not using!

Health Saving Accounts 101

Most people strictly associate Health Savings Accounts (HSAs) with savings that can be used on health coverage and medical expenses. While HSA’s cover qualified healthcare expenses, they also can be used as a tax friendly vehicle for retirement savings. But first, let’s answer the basic questions about HSA’s:

- Plain language. What’s an HSA? A HSA is a tax efficient savings vehicle specifically designed to accompany a high deductible health care plan (HDHP).

- Do I qualify for an HSA? If you have a HDHP, then congratulations! You qualify for an HSA.

- What qualifies as a “high deductible” health insurance plan? A HDHP is a plan with an annual deductible of at least $1,350 for an individual (double that for a family).

- What do you mean by “qualified medical expenses?” Qualified medical expenses are your medical expenses not covered by insurance, including (but not limited to): ambulance services, prescriptions, doctors appointments, dental care, and vision care. Additionally, certain health insurance premiums, Medicare expenses, and long-term care insurance premiums are qualified as medical expenses for HSA use.

- Does my employer offer an HSA? For employee offered health insurance plans last year, 57% were offered a HSA. However, if you qualify for a HSA but your employer does not provide them, you can still open a HSA with a financial institution. Your financial planner help can guide you.

Healthcare Costs Are Expensive!

One of the biggest obstacles in retirement planning can be high health care costs, which continue to rise and are compounded by a variety of factors. In fact, the Center for Medicare and Medicaid Services, projects that the average growth in health spending will be even faster between 2016 and 2025 [than previously projected], driven by inflation in the cost of medical services, products and an aging population.

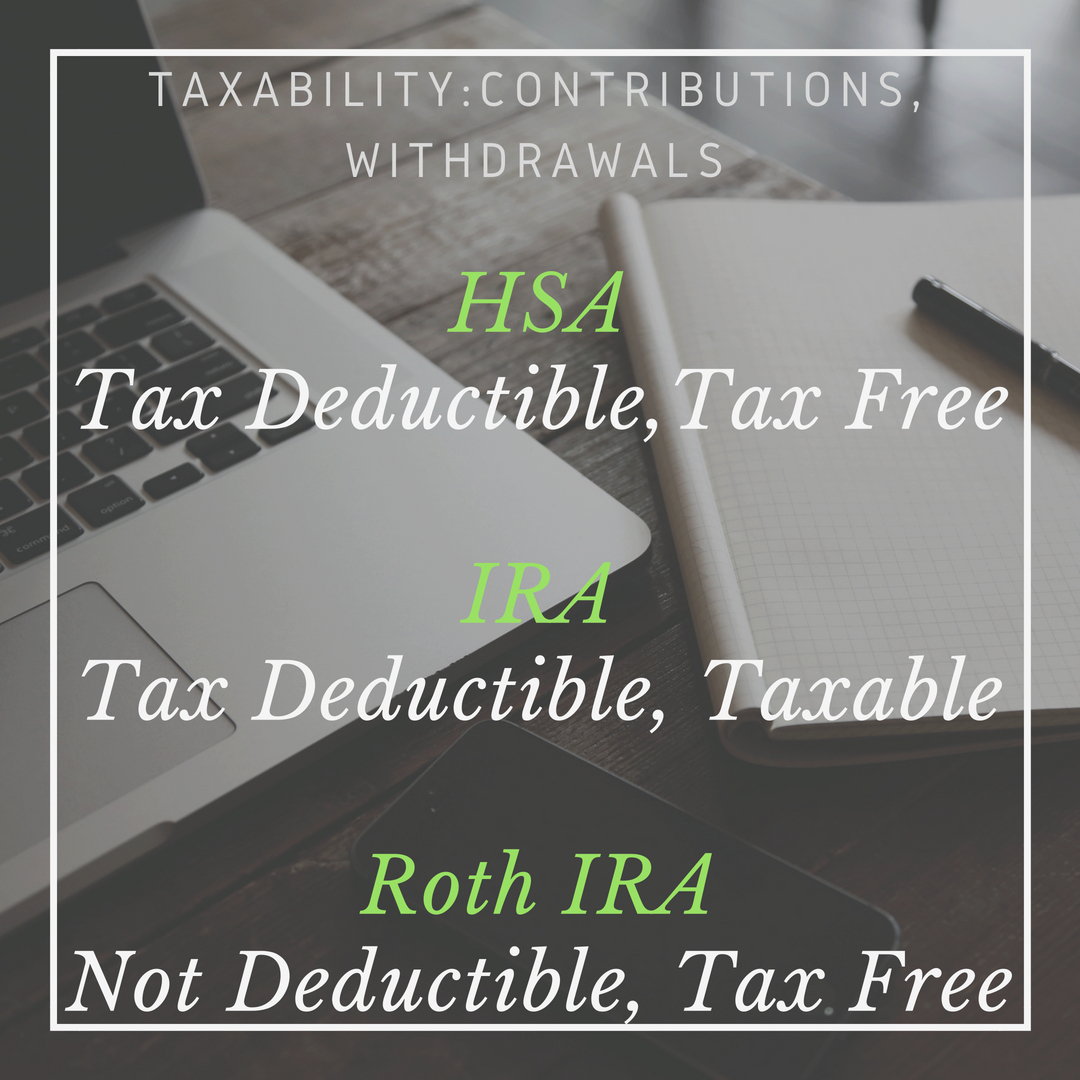

While there are many ways to plan for/save for future health expenses, HSA’s are one of the most tax efficient and underused methods. Contributions made to the HSA can be invested in mutual funds (just like your IRA); however, unlike other retirement savings accounts, HSA’s are tax efficient in all three phases: contributions, earnings AND distributions. All three phases are completely tax-free at the Federal level! This makes them even more attractive than an IRA or Roth IRA (see exhibit 1).

Exhibit 1

Now the Cool Part

I’ll let you in on a little secret: HSA’s can also be GREAT retirement savings accounts.

Until the account owner turns 65, the funds in an HSA can only be used to pay for qualified medical expenses. Withdrawals used for non-qualified medical expenses prior to this point are subject to income taxes and a 10% penalty. However, after the age of 65 or Medicare eligibility, withdrawals for non-medical expenses are no longer subject to the 10% penalty, though they are subject to income taxes (just as they would be from a traditional IRA). This feature allows many people to utilize their HSA as another retirement savings vehicle – especially because there is no income limits on contributions. Another factor that has made HSA’s popular is that the distributions (tax-free, I remind you) are not required to be taken (unlike a required minimum distribution from an IRA or 401(k)). As a Financial Advisor, “tax-free” and “no required minimum distributions” are two ways you can always make me smile.

I’ll leave you with one last thought… there are a few concepts I am personally passionate about: maximizing savings, tax efficiency and ensuring health expenses are financially accounted for in planning. If you have had relatively low health expenses the past few years, and do not foresee any major increases on the horizon, right now is the time to evaluate the effectiveness of how your utilizing your HSA.