Written by: Mark Rylance (May 2022)

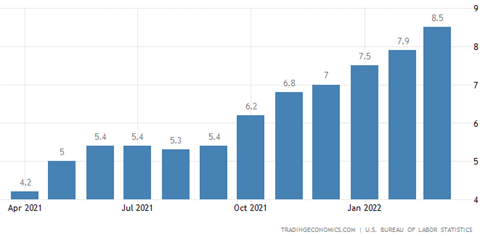

A lot has transpired since our last update letter in March. At that time, the focus was on Ukraine and inflation. Now, the focus seems to be square on the economy and inflation. Late last year, the Fed referred to inflation as “transitory”, thinking that it would quickly pass through. But as you can see in the chart below, inflation is far from temporary. The chart below shows the progression of inflation over the past twelve months.

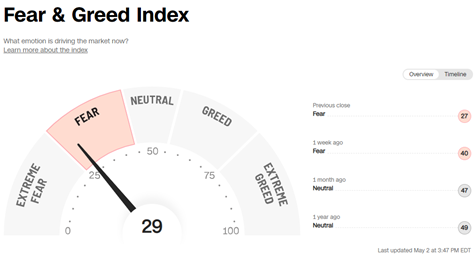

Global bond and stock market declines have combined to create a very anxious environment for investors. That said, we wanted to provide you with some thoughts and information to help counteract some of the negative headlines you may have read or may be reading in the future. We have previously referred to CNN’s Fear & Greed Index in the past—here is where it currently stands. Keep in mind that “fear and greed” sell a lot of newspapers and advertising, so you should always be aware of the power and influence of media headlines, and its effect on our emotions.

MORE ON INFLATION

Once thought to be a temporary nuisance in the form of higher gas prices late last year, inflation has now permeated every aspect of our lives from food, rents, airfares, and everything in between. Inflation has taken form in both higher prices, as well as “shrinkflation”. Shrinkflation is when your box of Oreos has 15 cookies instead of 20. Whichever form of inflation, it has become sticky and will be with us for quite a while longer, possibly extending into next year. We do believe inflation will begin cresting in the next few months but do not expect much relief any time soon. And remember, when inflation goes down it doesn’t necessarily mean that prices will go down, it just means the rate of change goes down.

We do feel that inflation will be peaking in the months to come, but it will remain high for the remainder of this year and possibly into next year.

What has caused all this inflation? The answer is complicated, but it has been driven by a combination of supply disruptions resulting from Covid shutdowns, labor and material shortages, and the trillions of stimulus money injected directly into the pockets of consumers. The $4+ trillion in Covid spending was successful in creating 20+ million jobs, but it also created ravaging inflation that is now affecting 180 million Americans. Sadly, inflation takes the form of a hidden tax that hits lower and middle-class families the hardest. Was it worth it? We’ll let the politicians sort that out.

THE FED

Prior to March, most economic pundits didn’t expect Fed Chairman Jerome Powell to get serious about combating inflation. He has a history of flip flopping when markets start heading South. Many thought he would talk tough but keep the throttle on the easy money machine. The consensus feels that this is no longer the case. The Fed has made the decision to raise interest rates aggressively and end their decade long money printing strategy (quantitative easing).

Strong words have been coming from many of the Federal Reserve Governors, including Fed Vice Chair Lael Brainard, who said a few weeks back that the Fed will “begin to reduce its nearly $9 trillion balance sheet quickly, arriving at a considerably more rapid pace of runoff than the last time the Fed shrank its balance sheet”. This means that not only will they stop purchasing $120 billion of US treasuries and mortgage-backed securities per month, but now they will begin reducing the supply of treasuries and mortgage-backed securities. This is important because these activities have been a primary driver of the artificially low interest rates over the last decade.

For the record, the last time the Fed raised interest rates while reducing its balance sheet was December of 2018, when the S&P 500 dropped nearly 20% in one month. The recent market sell-off is not surprising given how much more leveraged the U.S. economy is now compared to 2018. For those wondering, the Fed does not have a good track record of engineering soft landings during tightening (raising rates) cycles.

MARKET REACTIONS

Markets have begun testing Powell’s resolve. Global stock and bond prices are pricing in interest rate hikes and an economic slowdown, but probably not a recession yet. The Nasdaq was down 13% in April and is down over 20% for the year. The S&P 500 was down 9% in April, and year-to-date is off to its worst start since 1939. The Bloomberg US Aggregate Bond index is also down over 10% for the year.

INFLATION AND BONDS

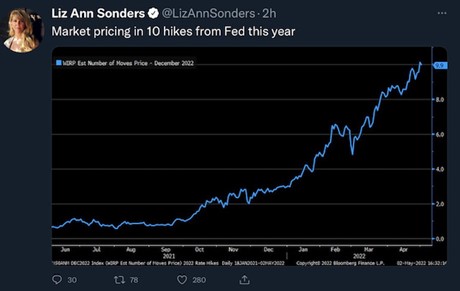

The bond market now believes the Fed will follow through on their tough inflation talk and has priced in another 10 quarter point increases before the end of 2022 as seen below. This would take the Fed funds rate to just under 3%. The new “hawkish” stance sent the bond market spinning as bond vigilantes proceeded to price in the rate hikes, leading to bonds having their worst quarter since the 1980’s.

All bonds were affected, not just the more volatile longer-term and lower rated bonds. We (RS Crum) were intentionally positioned with all high-quality bonds and ultra-short durations, but there were still no places to hide. Thankfully we had also reduced 20% of our bonds over the last year and redeployed the proceeds across several alternative investments, some of which have paid off handsomely.

The good news is that the 10-year treasury yield now seems to have hit its upper range, which means the rate is matched with inflation expectations 10 years from now. The current yield on the 10-year treasury touched 3% this week while the 10-year annualized inflation rate expectation is 2.8%. Bond prices typically move in lock step with future inflation expectations.

If inflation starts to settle and slowly begin reversing, bond prices should stabilize. We have also seen shorter-term bond yields rise to 2.75%, which should start attracting money flows, and also help stabilize bond returns.

INFLATION AND STOCKS

Unlike bonds, stocks are affected by many more factors than just interest rates and inflation expectations. Stock prices are most influenced by future earnings growth expectations. If earnings grow more than expected stock prices should follow suit. However, that is not always the case in the short-term. There can be extended periods of time where stock prices rise by more than their earnings. The transition from low inflation to high inflation, and low interest rates to higher rates, may put more focus on earnings going forward. As Netflix and Amazon just learned, if a stock is priced for high growth, but doesn’t deliver, the market can be ruthless.

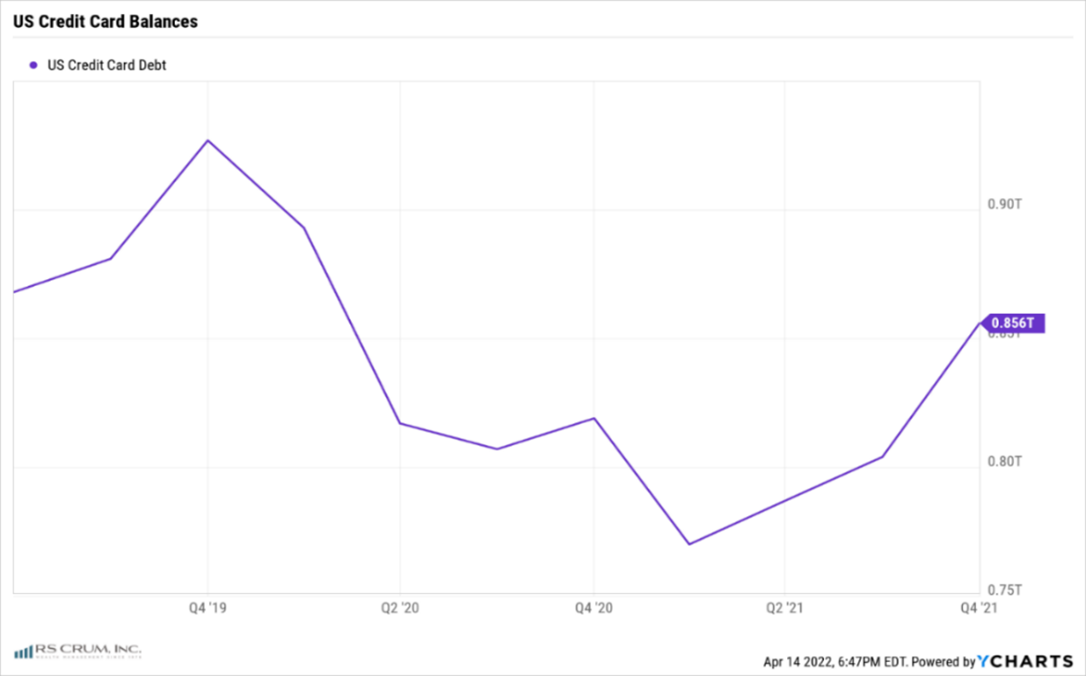

In addition to the many challenges facing companies around the world, the world will need to adapt to a new environment without Covid stimulus money. Consumers, who have been flush with cash the last few years are now starting to build up credit card balances. Such balances have increased 10% in just the last year. We are not at pre-Covid levels yet, but the trend is something to keep an eye on.

At the beginning of the year analysts predicted that the S&P 500’s earnings would grow by 10% in 2022. We mentioned earlier this year that we thought this was too optimistic given the headwinds public companies faced in 2022. We felt that rising material and labor costs, supply chain issues, Covid shutdowns (i.e. Asia), high oil prices, and slowing consumer spending would all combine for increased uncertainty. Most companies are revising their expectations for the rest of the year, and the markets are adjusting accordingly.

INFLATION AND REAL ESTATE

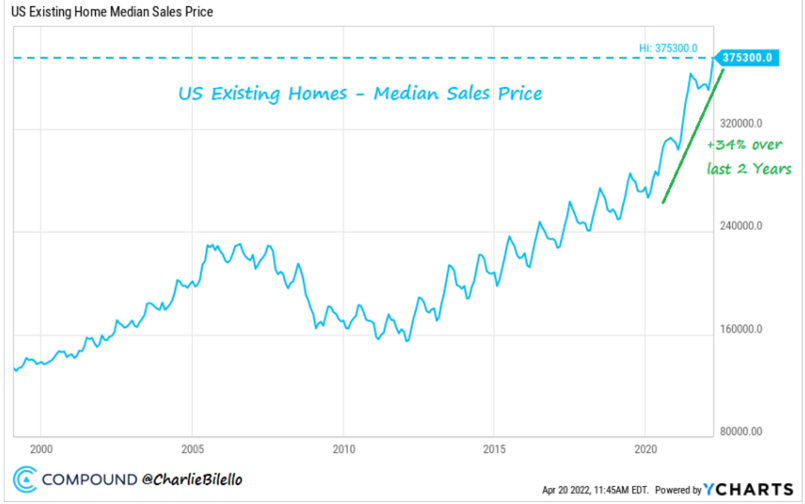

According to Freddie Mac, the average 30-year mortgage rate is now at 5.11%, up 67% in the last 12 to 18 months. This has started to cause a cooling effect on an otherwise historically “hot” housing market. Redfin reported that the typical homebuyer’s monthly mortgage payment is now 39% higher than last year, the largest increase on record. If you factor in the 20% increase in home prices, the cost of buying a house is up roughly 50% year-over-year. Their data also suggests that buyers are starting to take a step back, with pending home sales down 8% from last year. This will likely accelerate in the month of April.

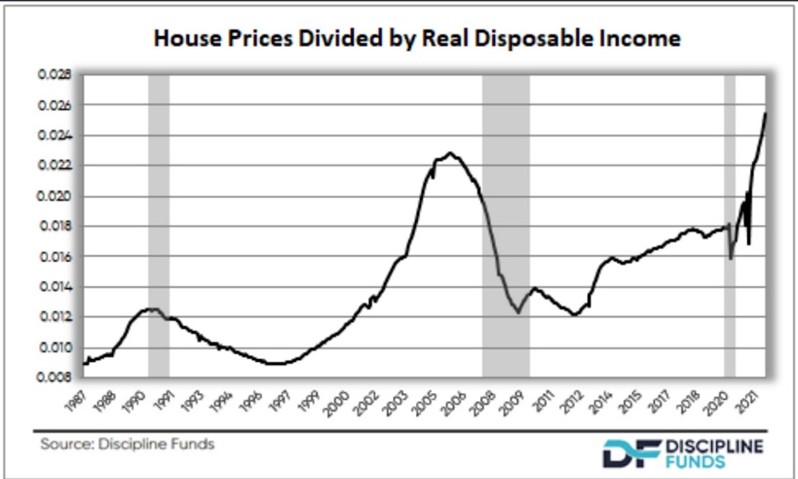

As seen in the chart below, housing prices are at an all-time high and affordability is now at an all-time low.

The slowdown in housing is welcomed by the Fed. There is a wealth affect associated with housing prices. If people feel less wealthy, they tend to spend less.

THE ECONOMY

Raising rates and removing monetary stimulus is a challenging path to take at any time but attempting to do both in a slowing economy, is downright dangerous. GDP in the first quarter of 2022 contracted -1.4%. The government blamed Covid restrictions and reduced government assistance programs for the negative GDP number. Even with the negative GDP number, American households kept spending at a 2.7% higher rate from a year earlier. Companies also kept pace, with capital spending rising 9.2% in the first quarter.

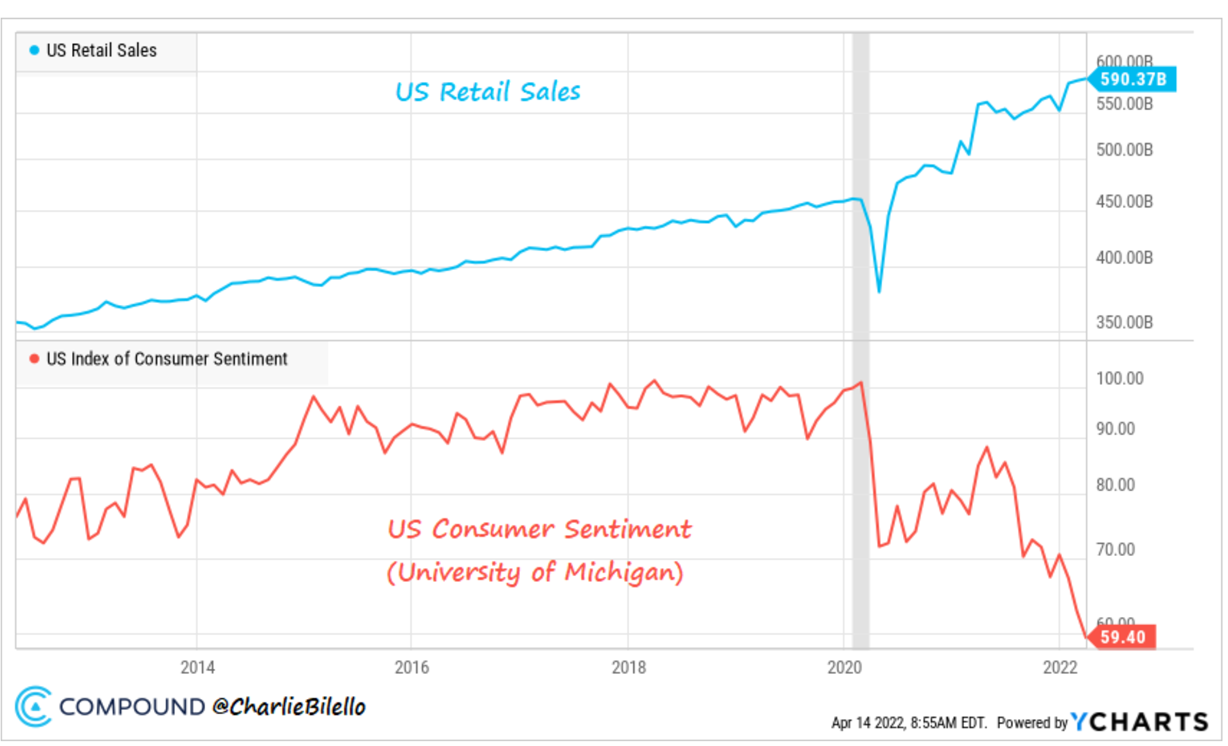

Even with spending strong, there is still a shroud of doubt between how people feel and their current spending habits. The chart below shows the discrepancy between spending and consumer sentiment. This spending could be a continuation from the pent-up demand coming from the Covid lockdowns.

SLOWDOWN OR RECESSION?

Are we headed for a recession? This is the question we have been asked most by clients.

It’s still too early to tell how much the economy will slow, but companies are starting to get a little uneasy. Corporate earnings have been solid so far, with a majority beating their estimates. However, their forward guidance has been cautious at best.

Gary Friedman, CEO of Restoration Hardware recently told Steve Forbes “…I don’t think anybody really understands what’s coming from an inflation point of view, because either businesses are going to make a lot less money or they’re going to raise their prices. And I don’t think anybody really understands how high prices are going to go everywhere.”

He goes on to talk about the cost of shipping doubling and then some. That is if you can find containers. And once the containers do arrive in port, good luck finding a truck to take the goods to their destination.

So, something must give.

Either corporations will be successful in raising their prices, or consumers will start spending less. The Fed’s hopes for a “soft landing”, effectively slowing consumer demand (spending) until supply constraints normalize. They want to accomplish this while avoiding the popping of the asset bubbles (that they created) in the stock, bond, and real estate markets. Oh, and they also need to avoid a recession and high unemployment. We previously called this the tightrope walk across the Grand Canyon.

IN CLOSING

We realize that this report is not going to give you a warm and fuzzy feeling. It is not our intention to stoke fear or other negative emotions, but rather to give you an honest assessment of the current situation. As much as we would like to avoid temporary investment losses, we feel a reset of the economy might be necessary to get us back to a healthy functioning economic system.

Our government has made a slew of policy errors over the last few years and now we are paying the price. Unfortunately, this fight should have started a year (or more) ago. We believe that attacking inflation is the right move because, if unaddressed and allowed to continue, a worse outcome might emerge – high inflation with slow growth (aka “stagflation”).

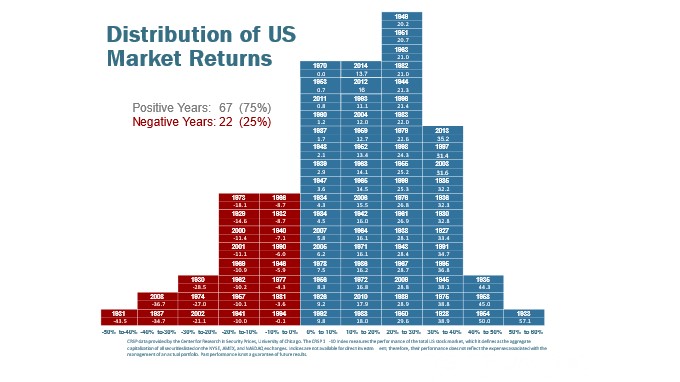

Please remember that markets are fluid and never stay down for long. If we do enter a recession, we should be prepared for even more volatility. But as always, it’s temporary. The chart below is a little out of date, but it illustrates an important concept. Even with stocks earning over 10% per year over time, 25% of the time they post negative returns. This is normal.

The chart also demonstrates how stocks reverse course quickly. After declining more than 40% from 2000 to 2002, the S&P 500 followed up with positive returns of 32% (2003) 12% (2004), 6% (2005), and 16% (2006). After the “great recession”, stocks returned: 29% (2009), 18% (2010), 0.8% (2011), 16% (2012), 35% (2013), continuing that positive run all the way to 2020 when the pandemic hit.

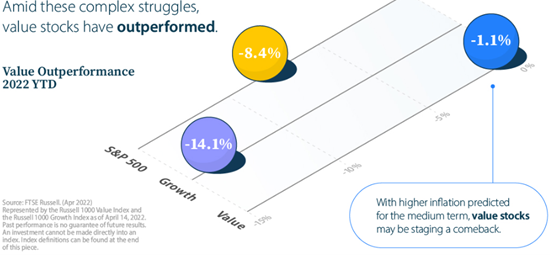

We feel that we have your investments positioned well. Our inflation hedges have worked well, and our leaning towards value stocks have paid off as can be seen below. Nobody likes seeing losses, but in markets like this, the name of the game is reducing losses and positioning for the rebound when it happens.

We will maintain our discipline and continue looking for opportunities to efficiently rebalance your investments at the appropriate time. We will also carry on with our tax-loss-harvesting work, booking losses to help offset gains in the future.

As we navigate this challenging time, please know we will do our best to communicate our thoughts on a regular basis. And if you have any questions or concerns, please don’t hesitate to reach out to us any time.